By Oleksandr Molchanov

The transition from the total enterprise value, which is calculated, for example, by multiplying a multiplier by EBITDA, to the purchase price (equity value) is achieved by deducting net financial liabilities from the total purchase price. The delineation of liabilities that belong to net financial liabilities often proves to be a contentious issue in the context of purchase price determination in corporate transactions.

In addition to less controversial components of net financial liabilities, such as bank liabilities or loans, there are other issues whose definition is not trivial.

In this article, we want to talk about the item that most frequently gives rise to discussion—lease liabilities.

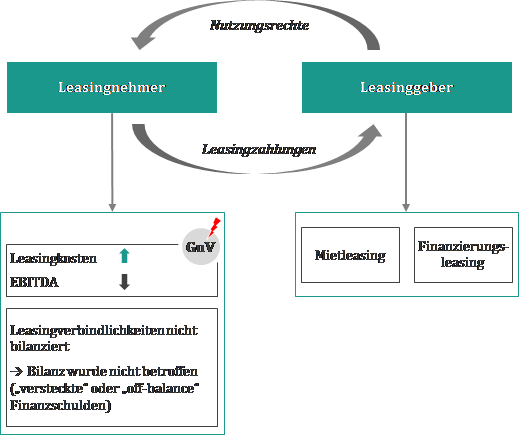

According to the HGB standard, lease liabilities are not recognized in the balance sheet. This means that the lessee’s balance sheet is not affected by the lease liabilities. These only appear in the form of leasing costs on the profit and loss side.

Figure 1

Since lease liabilities are not recognized as liabilities, they are referred to as “hidden” or “off-balance” financial liabilities.

Lease liabilities are interest-bearing debts and should be deducted from the total enterprise value as part of net financial liabilities, thereby reducing the purchase price. Since the leasing costs to be borne reduce the operating result (EBITDA), which is not the case with traditional bank liabilities (interest costs appear under the item “Interest and similar expenses” and therefore have no impact on EBITDA), caution is advised when determining the purchase price.

If the lease liabilities are simply deducted from the total value of the company, the seller is “doubly penalized” – on the one hand by the impact of the lease liabilities on net debt and on the other hand by the burden on EBITDA due to the leasing expense, which leads to a lower valuation of the target company. If the leasing liabilities have an impact on net debt and thus reduce the purchase price, the leasing expenses should always be fully deducted from EBITDA. In other words, EBITDA should be normalized or adjusted for the leasing expenses. Normalizing EBITDA increases the valuation basis accordingly.

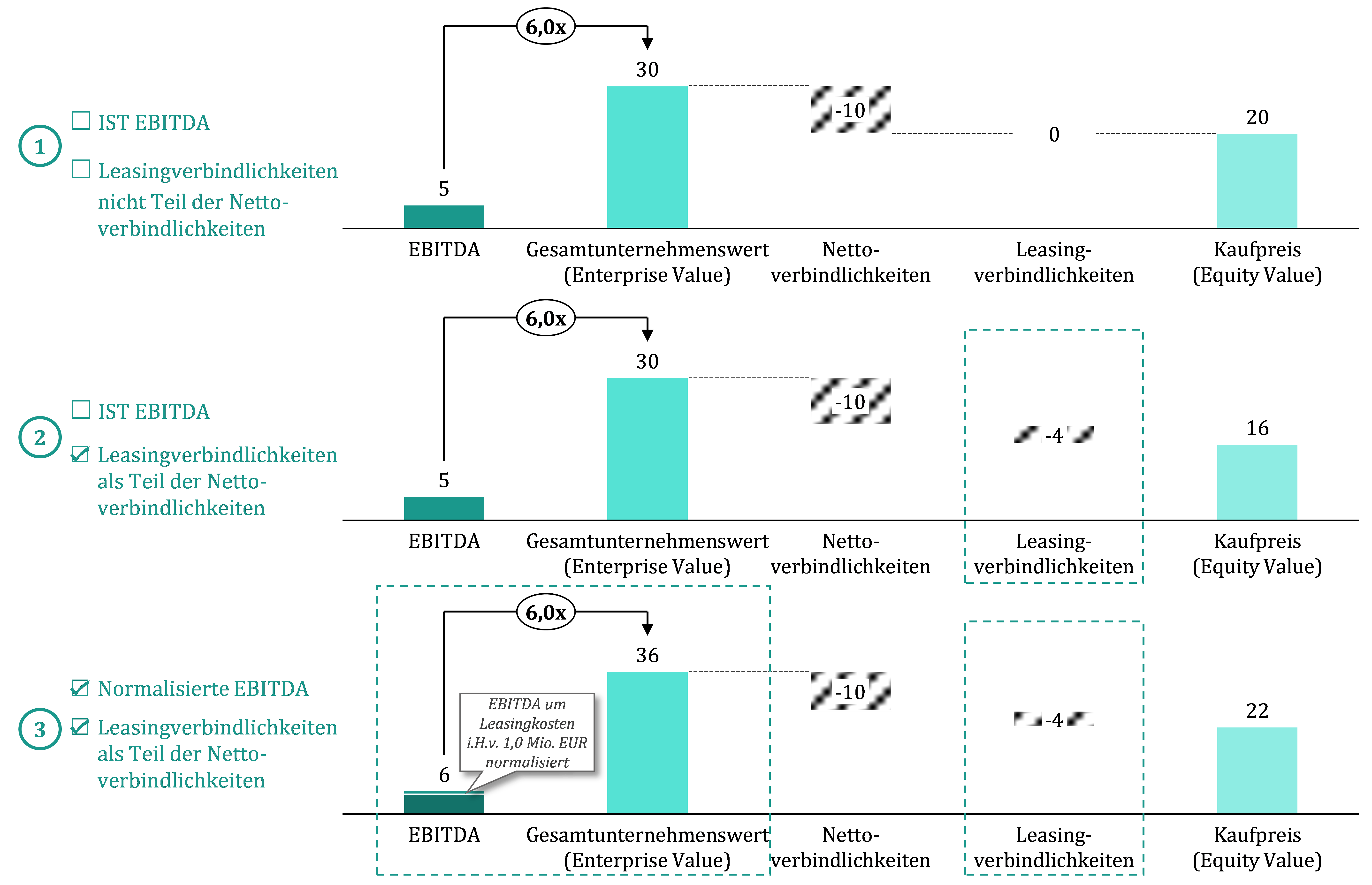

Parameters of the example:

EBITDA: EUR 5 million

Leasing costs: EUR 1 million

Net liabilities (excluding lease liabilities): EUR 10 million

Lease liabilities: EUR 4 million

EBITDA multiplier: 6.0x

Figure 2

The example shows how the purchase price can change if the lease liability is included in the purchase price mechanism with or without normalization of EBITDA – the difference is EUR 6 million when applying the same valuation multiple.

The inclusion of lease liabilities in the purchase price calculation for a company sale (or purchase) has great potential for dispute. Due to the variety of possible factors to be taken into account, an individual analysis of the transaction object is necessary in each case. Awareness of the various factors and their interactions with the balance sheet and income statement items, as well as the development of convincing arguments, form the essential basis for successfully enforcing negotiating positions.

Your contact:

Philip Herrmann, Director

Tel. +49 531 180 59 300

E-Mail: mailto:info@i-capital.de

Oleksandr Molchanov, Senior Consultant

Tel. +49 531 180 59 360

E-Mail: mailto:o.molchanov@i-capital.de